The traditional 4% rule no longer works for today’s retirees. Learn how inflation, longer

lifespans, and Social Security strain are reshaping retirement in Tacoma — and how the

Financial Minimalist Plan creates stability through dynamic cash flow, not guesswork.

Discover how amortization really works, how banks use timing to profit from your payments, and how Tacoma homeowners can reverse the flow to save thousands in interest and years off their mortgages.

Discover 8 warning signs that your money controls you instead of the other way around. Learn how Tacoma families can build freedom through flow, timing, and structure — not sacrifice.

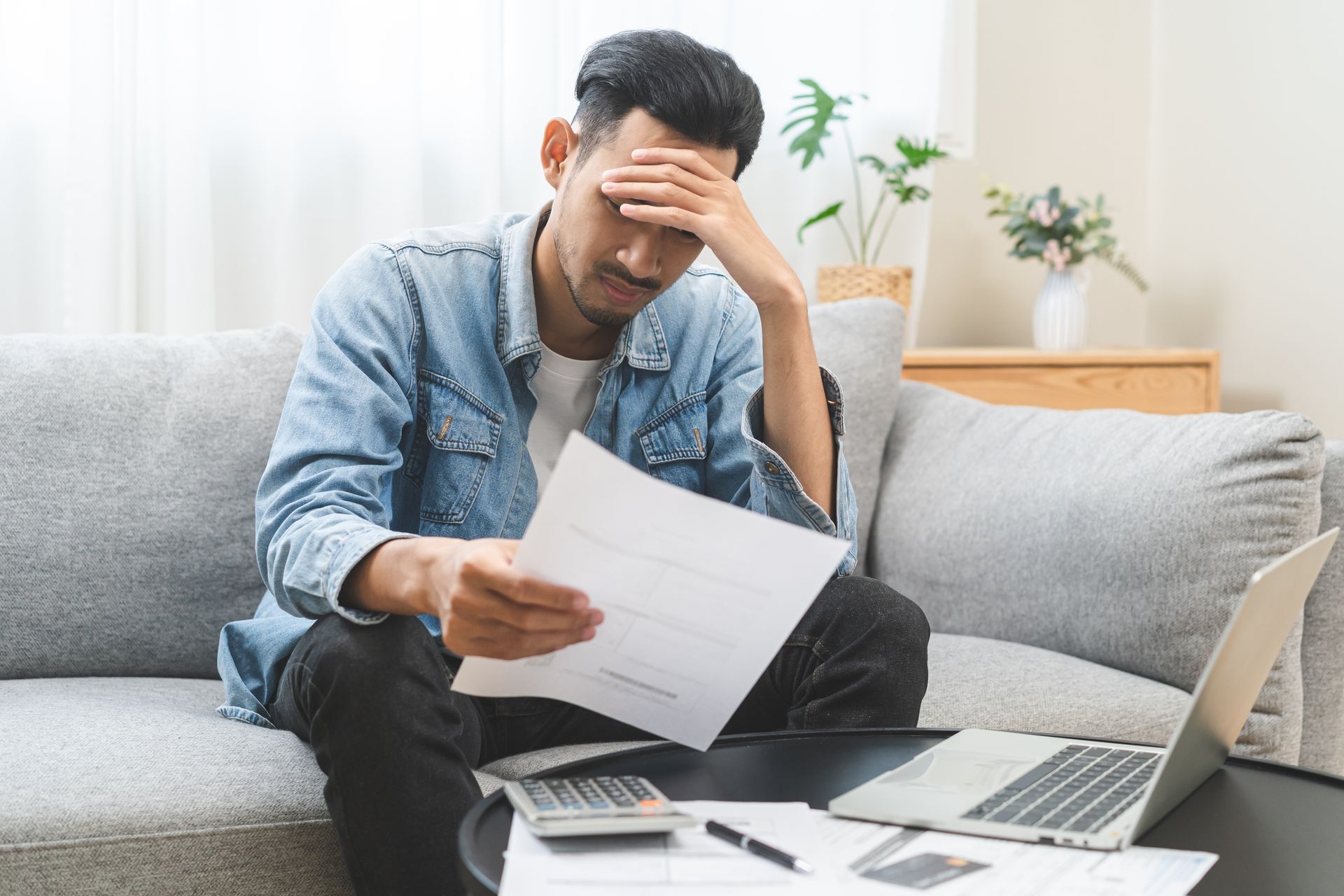

Learn how to recognize when your debt payoff strategy is broken. Tacoma families are

discovering faster, smarter ways to eliminate debt through structure — not sacrifice.

Learn the overlooked ways Tacoma families lose thousands each year — from interest traps to convenience spending. Discover how to reclaim your money through structure, timing, and smarter flow.

Learn which common financial rules hurt Tacoma families the most — and how to replace them with smarter structure, timing, and flow through the Financial Minimalist Plan.

Learn the signs that your money isn’t working for you — from refinancing traps to unstructured debt. Discover how Tacoma families are using the Financial Minimalist Plan to make every dollar move with purpose.

Discover the truth behind the most common debt myths that keep Tacoma families trapped for decades. Learn how the Financial Minimalist Plan helps you eliminate debt and build wealth — at the same time.

Discover nine lessons about money, structure, and timing that most people in Tacoma learn the hard way. Avoid common traps and start building freedom faster with the Financial Minimalist Plan.

Even high earners in Tacoma struggle with money because of hidden habits that drain wealth. Learn the top 10 behaviors keeping families stuck — and how to break free through better structure and flow.